Kiwi startup funding rebounded in 2024 - NZGCP

New Zealand's startup ecosystem demonstrated significant recovery and growth throughout 2024, with both deal volume and investment amounts showing marked improvement over previous years.

According to the latest Young Company Finance report from NZ Growth Capital Partners (NZGCP), the Government’s investment vehicle for supporting early-stage companies, total investment across the sector reached $466.8 million in 146 successful funding rounds in FY 2024, representing a substantial 34% increase compared to 2023.

Key investment trends

The second half of 2024 proved particularly strong, with investment levels significantly outpacing the same period in 2023. Total investment in H2 2024 surged by 101% compared to H2 2023, while the number of deals increased by 29%. This growth was driven by eight deals exceeding $10 million in round size - four times the number seen in H2 2023.

Source: NZGCP

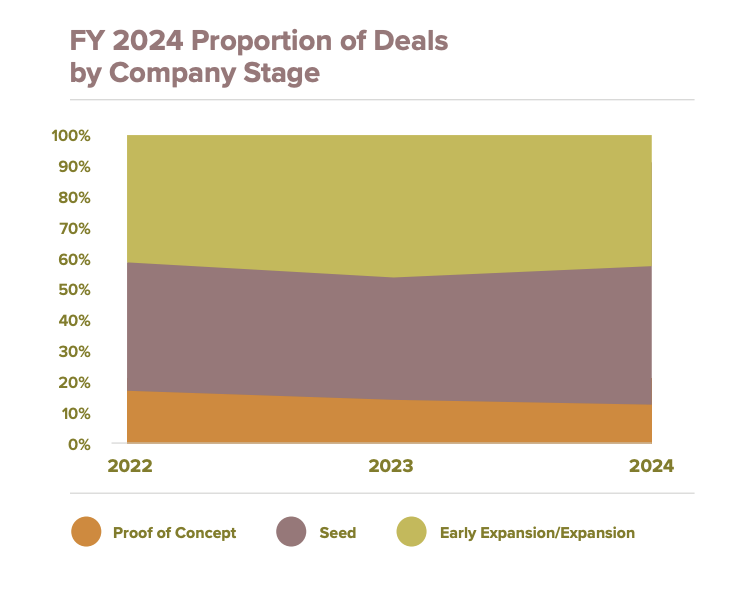

Seed-stage companies dominated the funding landscape, accounting for 45% of all transactions in FY 2024. This demonstrates continued investor willingness to back early-stage startups, an essential component for long-term ecosystem health. Notably, seed investment nearly doubled compared to the previous year, reaching $124 million in FY 2024, up from $63 million in 2023.

“It is against this backdrop that we remain optimistic about the emerging trends in our ecosystem,” wrote Jacques Richter, Associate Investment Director at NZGCP, in an introduction to the report.

“In our last report, we noted increasing confidence in the sector and the emergence of green shoots. Despite subdued activity in H1 2024, decreasing interest rates and lower inflation

fuelled investor appetite for early-stage investments.

“Increased liquidity was evident in the return of mergers and acquisitions (M&A) activity, with some notable exits enabling investors to return or recycle capital back into the pipeline of emerging start-ups.

“The second half of 2024 proved to be more buoyant, with investment levels up from 2023 - both in terms of the number of deals and total capital invested. However, absolute activity

levels remain low for a country of our size, and much more needs to be done to amplify this sector and unlock its vast potential for positive impact on the broader economy,” Richter wrote.

New deal activity rebounds

One of the most encouraging signs was the significant rebound in new deals during H2 2024, with 30 new deals completed - more than double the 14 recorded in the same period of 2023. This took the total number of new deals for FY 2024 to 36, representing a 20% increase on FY 2023, though still below the five-year average.

Total investment in new deals also saw impressive growth, reaching $45 million in H2 2024 - up from just $20 million in H2 2023. Despite this improvement, the share of new deals compared to follow-on deals (25% in FY 2024) remains below the historical average of 35%.

Shifting investment landscape

The landscape of lead investors has undergone a significant transformation, with venture capital funds now comprising 58% of total deals, while angel investors account for 37%. This shift reflects changing dynamics in the investment ecosystem, with the share of venture capital investment rising dramatically from just 8% in 2019, when the Elevate NZ Venture Fund was established.

Early Expansion/Expansion stage investments saw particularly strong growth, surging to $271 million in H2 2024, more than doubling from $121 million in H2 2023. For the full year, this category rose to $319 million, up from $268 million in FY 2023, fueled largely by Pre-Series A ($96 million) and Series A ($134 million) investments.

Source: NZGCP

“Encouragingly, seed investment has seen substantial growth, nearly doubling compared to

the previous year. This demonstrates that investors are still willing to back early-stage start-ups, an essential component of long-term ecosystem health,” wrote Bridget Unsworth from the Angel Association of New Zealand, in the report.

“However, the funding landscape remains weighted toward follow-on rounds rather than new deals, suggesting that while existing companies are securing continued support, more

momentum is needed to fuel the next wave of start-ups. A sustained increase in new deal activity will be crucial for maintaining a steady flow of innovation and ensuring long-term growth,” she added.

Regional and sector distribution

Geographically, activity remained consistent with previous years, with Auckland, Wellington, and Christchurch accounting for 81% of total deals in FY 2024. Auckland's total investment amount grew by 13% compared to FY 2023 and saw an 85% increase from FY 2022. The Canterbury region reached $42 million in investment, nearly doubling its previous recorded high, with multiple large funding rounds between $8 million to $12 million.

Sector-wise, Software startups rebounded strongly in H2 2024 with 47 deals, compared to 29 in H2 2023. Software continued as the lead sector, representing 48% of total investment across all sectors and 46% of total investment for FY 2024 - a significant increase from 27% in FY 2023.

Clean-tech and Health-tech sectors maintained steady growth, collectively accounting for 28% of all deals in FY 2024, up from 20% two years ago. However, their share of total investment declined to 33%, down from 48% the previous year, due to the surge in Software startup investment.

Some notable divestments

2024 was a strong year for startup exits, according to NZGCP. During H2 2024, the local start-up ecosystem released capital back to early-stage investors such as the investment into Kami by Boston Ventures and the acquisition of Tradify by the Access Group and early on in 2025 notable acquisitions were announced for Robotic Plus and Quantifi Photonics

The outlook for 2025 and beyond

While these positive trends signal strong recovery and renewed investor confidence, challenges remain, particularly in increasing new deal flow beyond the five-year average.

As noted by industry experts, a more robust pipeline of fresh investments will be essential to maintaining long-term ecosystem vitality.

Nevertheless, the market's trajectory is promising, with strong investment activity laying the foundation for further expansion in New Zealand's startup ecosystem.